Third Quarter 2019 Commentary

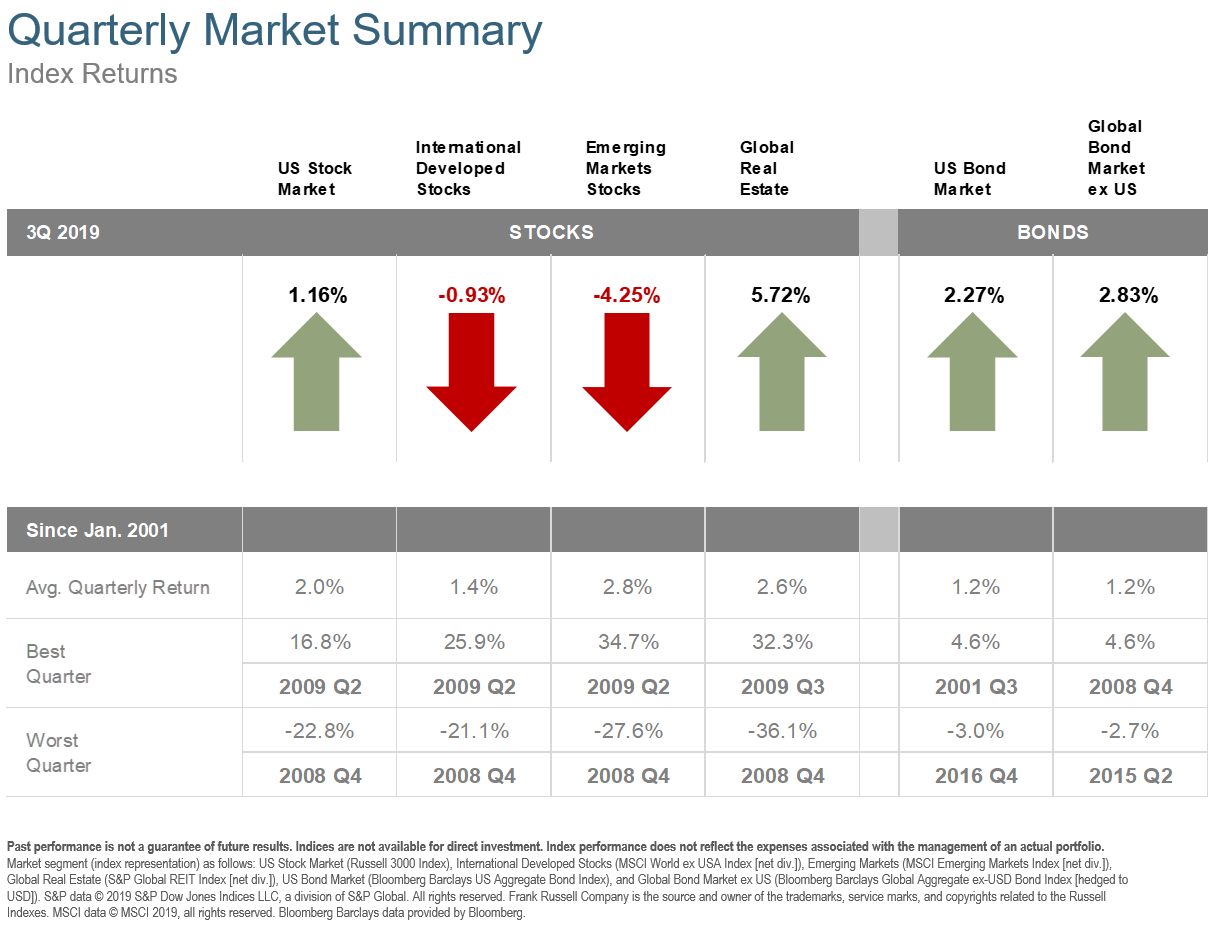

The third quarter had no shortage of big headlines but not much has fundamentally changed. U.S. stock performance was slightly positive, while international developed markets were slightly negative. Emerging markets and global real estate had larger swings with the former down over 4% and the latter up almost 6%. With interest rates continuing their decline, U.S. and global bonds both performed well this past quarter.

The U.S. economy grew at an annual rate of 2% in the second quarter. Inflation increased 1.7% for the 12 months ending in August. The unemployment rate decreased to a 50-year low of 3.5%. While the U.S. economy continues to generate positive results, global trade and U.S. Monetary policy remain key issues.

Global Trade

At the end of the second quarter, it seemed that the trade talks between the U.S. and China were moving in a positive direction. Unfortunately, things escalated during the third quarter with additional tariffs being applied from both sides. Talks are expected to resume later this month. While the U.S. and China receive the headlines regarding this trade war, almost all countries are affected. For example, Germany’s GDP decreased 0.1% in the second quarter. Much of the slowdown in their exports is attributed to reduced demand from China.

Elsewhere in trade, the United States-Mexico-Canada Agreement (USMCA) will potentially be approved by Congress during the 4th quarter. The U.S. will begin applying tariffs on certain European Union (EU) goods later this month in retaliation for illegal aircraft subsidies provided from the EU to Airbus.

U.S. Monetary Policy

The Federal Reserve reduced interest rates twice during the third quarter. While the unemployment rate remains low and the economy continues to steadily grow, this was seen as an “insurance” cut in response to low inflation, global weakness, and trade tensions. The 10-year treasury bond rate declined from 2% to 1.69%. Buying longer maturity bonds at these high prices and low yields may benefit investors if rates fall further or if we go into a recession but comes with significant risk if interest rates or inflation were to increase.

Conclusion

While the U.S. economy seems to be continuing its slow and steady expansion, growth is slowing in the rest of the world. That doesn’t mean the U.S. economy will follow suit, but it does warrant caution. The Federal Reserve is trying to accommodate for this uncertainty by reducing interest rates preemptively. This can have a positive effect, but high interest rates weren’t the cause of this slowdown. Ultimately these trade deals need to be completed so companies can go back to business as usual.