Second Quarter 2022 Commentary

As we enter the second half of the year, investors continue to grapple with inflation, higher interest rates, the Fed, and the prospect of a recession. If historical bear markets are any indication, the decisions investors make during this period will have long-lasting effects on their portfolios. Resisting the temptation to overreact to daily market swings, dwelling on the past, and losing sight of bigger factors has never been more important. While it's difficult to imagine a market recovery today, more than a century of market history suggests that they can occur when investors least expect. Investors should consider what will matter to markets over the next several months as they position for the years and decades ahead.

The stock market officially fell into bear market territory in June with the S&P 500 losing as much as 23% on the year before recovering somewhat. Last month alone, the S&P 500, Dow and Nasdaq fell 8.4%, 6.7% and 8.7%, respectively. The second quarter experienced the fourth-worst market performance since 1990, adding to a difficult first quarter. Interest rates climbed due to inflation and Fed rate hikes with the 10-year Treasury yield rising as high as 3.47%. Bitcoin ended the month down 41% to $18,731, continuing what many have dubbed “crypto winter.”

Bear markets are always difficult as anyone who invested through 2000, 2008 or 2020 can attest. However, experienced investors know that bear markets occur periodically and are an important part of each cycle. For those in a position to do so, these periods present opportunities to invest when valuations are attractive and position for future recoveries and growth. While the future is always uncertain, there is no doubt that all investors wish they had taken advantage of attractive prices during past bear markets. After all, the reason that investors are rewarded in the long run for owning stocks is the ability to stomach short-term uncertainty.

Below are several insights from the first half that will carry through to the remainder of the year. These include the relationship between stocks and bonds, inflation, the Fed, and more. Investors that can heed these lessons and stay disciplined will likely be better positioned to achieve their long-term financial goals.

Stocks and bonds have both struggled this year

What has made this year challenging is that both stocks and bonds have performed poorly. This is because the sudden jump in rates due to inflation has hurt all asset classes at the same time. This bucks the normal pattern of bonds supporting portfolios in difficult markets.

While infrequent, there are historical cases where similar patterns have occurred. The 1994 Fed rate hikes, the inflation worries in 1999, the 2013 taper tantrum and more were periods when rates spiked which hurt bond returns. In every one of these historical cases, interest rates eventually eased, and bonds recovered. While the current situation is unique, there are still reasons to believe that bonds are still an integral part of a balanced portfolio. Even now, recession concerns are already pushing interest rates down, restoring some of this historical relationship. This is why the most important principle of investing is still to stay patient and not try to time the market.

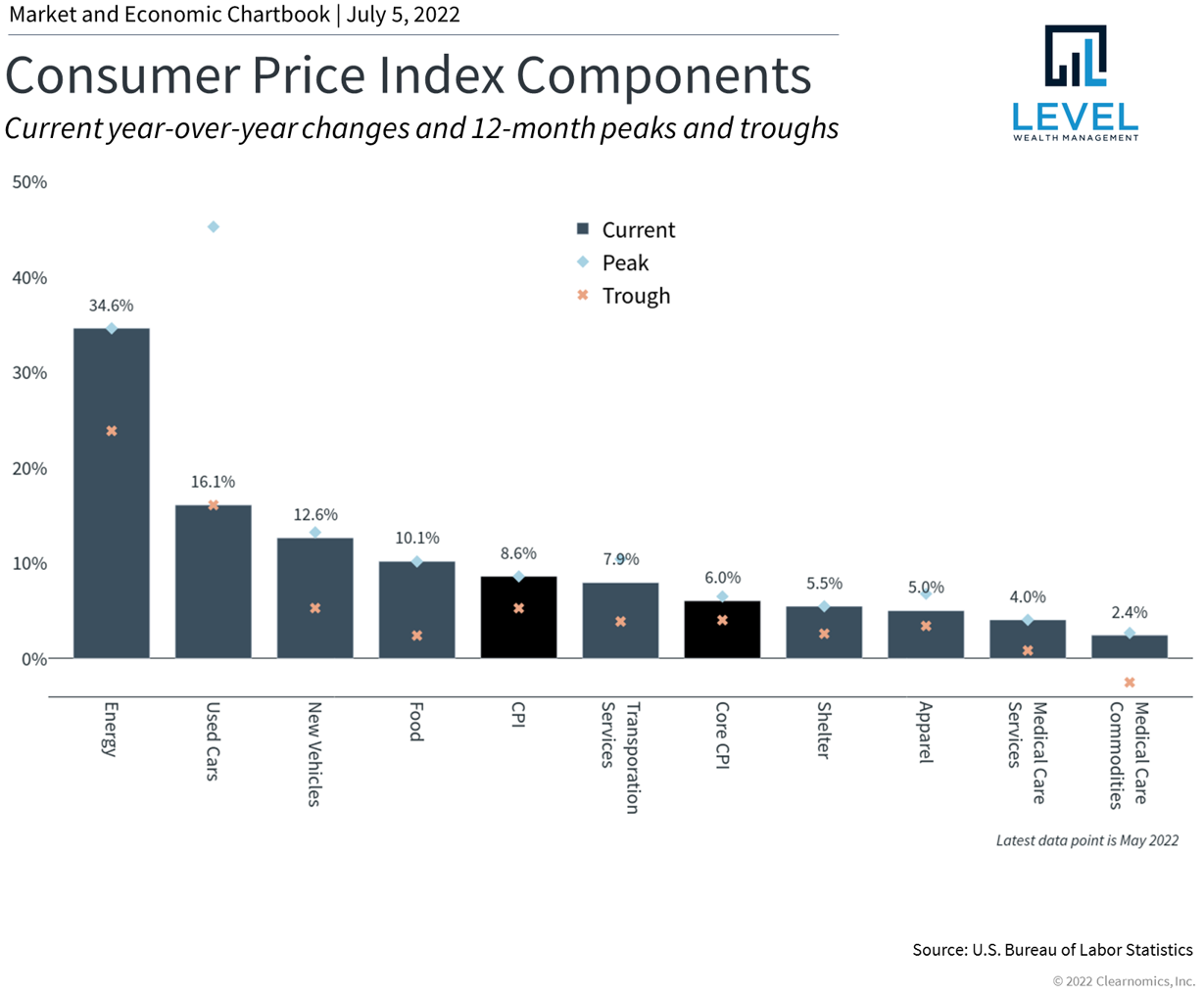

Inflation has increased across many categories

Inflation can be a tricky subject since it can be driven by many factors. Rising energy prices due to strong demand and the war in Ukraine have only made matters worse, especially for consumers at the gasoline pump. The fact that all prices have increased adds insult to injury and hurts consumer pocketbooks, reducing discretionary spending on other items. Recent data show that retail sales and spending have in fact declined.

In particular, gasoline prices near $5 per gallon has driven consumer confidence lower and raises expectations of higher inflation ahead. The primary determinant of gasoline prices is oil. This is why greater supply as geopolitics improve, and lower demand as the economy slows, could help to bring prices down in the second half of the year. If this happens, then inflation may begin to calm, and markets may find a reason to be optimistic in the months ahead.

Valuations present long-term opportunities for patient investors

Stock market valuations are at their most attractive level in years. Rather than being close to all-time peaks last seen during the dot-com bubble, the forward price-to-earnings ratio on the S&P 500 is now back to historical averages. For patient investors, this presents an opportunity to benefit from this downturn in the years ahead.

The Fed is tightening monetary policy

The Fed has ramped up its fight against inflation, stating that "the [Federal Open Market Committee] is strongly committed to returning inflation to its 2 percent objective" and "the Committee is highly attentive to inflation risks." While the Fed cannot directly solve the supply problems across a variety of industries, raising rates and tightening financial conditions can prevent runaway inflation by softening demand.

This is why the Fed has accelerated its pace of rate hikes with the May increase reaching 75 basis points (three-quarters of a percent), the largest in 28 years. The market expects similar rate hikes throughout the remainder of the year with the fed funds rate hitting about 3.5% by year end.

While bear markets are challenging, investors ought to view the current period with perspective. If inflation begins to ease, optimism may return to the market and economy. Taking advantage of the current market by staying invested and diversified are still the best ways to achieve financial goals in the years and decades to come.